See also

23.01.2025 11:23 AM

23.01.2025 11:23 AM

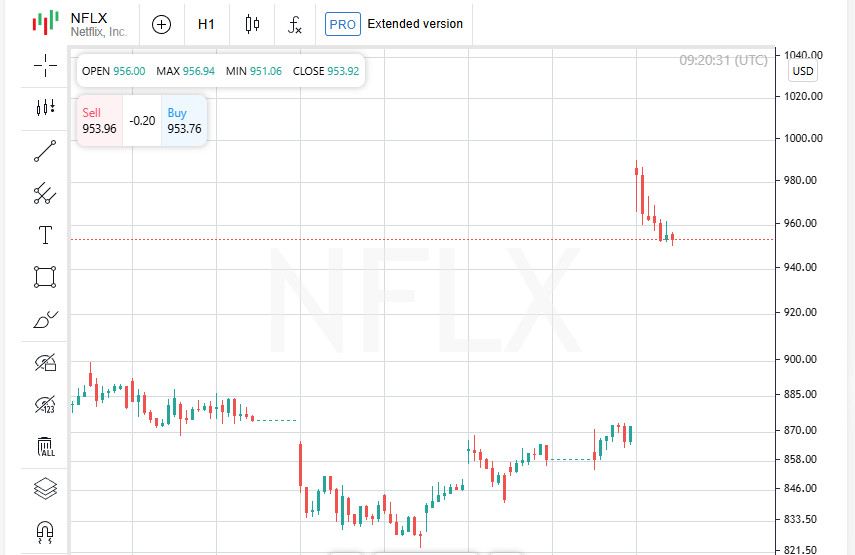

US stock indices showed solid gains on Wednesday, with the S&P 500 recording a new intraday high. The main drivers of positive dynamics were Netflix's strong financial results and Donald Trump's ambitious investment plan aimed at developing artificial intelligence infrastructure.

The tech sector posted an impressive 2.5% gain, leading the 11 major industries in the S&P 500. The surge was driven by gains from AI giants Nvidia and Microsoft, whose shares rose sharply in the session.

Netflix soared 9.7% on record subscriber growth during the holiday season. The results allowed the streaming giant to announce price increases on most of its plans, further bolstering investor confidence in its future.

Investors were enthusiastic after Donald Trump announced a major investment in artificial intelligence infrastructure. The new plan would see the private sector invest $500 billion, with major players including Oracle, OpenAI, and SoftBank taking part. However, the details of how the project will be funded remain unclear.

With technology and communications services gaining 1.1% on the day, other sectors performed more modestly. Utilities was the biggest loser, losing 2.2%.

Oracle shares jumped 6.8%, while ARM Holdings, a subsidiary of SoftBank and a key player in chip development, rose an impressive 15.9%. Server hardware maker Dell also showed steady growth, adding 3.6%.

Wednesday's results showed that investment in innovation and confidence in future technologies remain key drivers for investors, and markets are ready to support the trend towards artificial intelligence and high-tech solutions.

The S&P 500, Nasdaq and Dow Jones were again in the spotlight on Wednesday, continuing their upward trend. Leading indices showed confident growth on the back of positive economic data, easing inflation pressures and President Trump's cautious approach to tariffs.

The S&P 500 added 37.13 points (+0.61%), ending the day at 6086.37. Although the index was just a few points short of its record closing level of 1090.27 set in December, its dynamics continue to inspire investors.

The Nasdaq Composite confidently rose by 252.56 points (+1.28%) to 20009.34, breaking the important psychological barrier of 20 thousand points for the first time.

The Dow Jones Industrial Average increased by 130.92 points (+0.30%) and reached 44156.73.

Investors are showing optimism due to a number of factors:

However, traders remain wary. The president has already warned that tariffs on imports from China, Mexico, Canada and the EU could be introduced as early as February 1. This statement has forced analysts to revise their forecasts for the coming quarter.

Donald Trump has ordered federal agencies to prepare comprehensive trade reviews by April 1. According to Barclays experts, this date will be a critical benchmark for markets. If trade rhetoric intensifies, we can expect serious swings in investor sentiment.

Among individual companies, Procter & Gamble's report was a pleasant surprise. Shares of the consumer goods giant rose 1.9% after the company beat expectations for the second quarter. Demand for household products in the U.S. remains strong, supporting P&G's earnings.

Meanwhile, Johnson & Johnson was overshadowed. Despite the fact that the pharmaceutical giant showed results above expectations, shares fell 1.9%. Analysts attribute this to expectations of further pressure on the company in the face of increased competition in the sector.

Markets are in a state of anticipation: participants are watching new statements from the White House and the outcome of trade negotiations. At the same time, positive signals from companies such as Netflix and Procter & Gamble give grounds for optimism. As before, investors are ready to bet on the development of technology, growth in consumer demand and the adaptability of the economy in the face of global challenges.

After an impressive rally earlier in the week, sentiment in the markets has begun to change. Declines in individual stocks, disappointing forecasts and weakness in futures signal investor caution.

Ford was in the spotlight, losing 3.8% of its value after Barclays downgraded the stock. The decision was linked to expectations of a slowdown in the automaker's growth amid ongoing challenges in the industry.

Textron also disappointed the market, with shares falling 3.4% after it issued a 2025 profit forecast that was below analysts' expectations.

Halliburton was another loser, with shares of the oilfield services giant falling 3.6% after warning of weak activity in the North American market and publishing a downbeat quarterly report.

Investor sentiment remained largely negative on the New York Stock Exchange (NYSE), with 1.55 shares falling for every one that advanced. At the same time, 271 new highs and 57 new lows were recorded, highlighting the mixed bag of trends.

Global stocks, which had been rallying on the back of Donald Trump's ambitious AI infrastructure plans, began to lose momentum on Thursday. While optimism is fading, Chinese markets managed to stand out thanks to Beijing's support.

Enthusiasm over the huge investment in AI infrastructure is gradually giving way to realistic expectations, as investors begin to consider the risks and uncertainties associated with the implementation of such projects.

European and US stock futures point to a weak open.

These data reflect a continued cautious mood among investors, who are analyzing the possible consequences of changing market factors.

Current market dynamics indicate that investors are focusing on macroeconomic data, corporate reports and statements from world leaders. Forecasts for key companies and earnings expectations, combined with global economic uncertainty, will play an important role in shaping future trends.

Despite isolated signs of a slowdown, the market continues to demonstrate resilience, and the long-term outlook for key sectors remains attractive.

Global markets continue to react to key initiatives and statements that shape investor sentiment. Donald Trump's announcement of a colossal $500 billion investment in artificial intelligence infrastructure was a huge boost, but by Thursday the optimism was waning.

Trump's proposal includes giants such as Oracle, OpenAI and SoftBank, underscoring the seriousness of his intentions. The news initially sent a wave of enthusiasm through global stock markets. Indexes in the US and Europe, including the pan-European STOXX 600 and the US S&P 500, had hit new records in previous sessions.

However, the euphoria was overshadowed by other statements from the president: plans to impose a 10% tariff on Chinese imports have caused tension and introduced an element of uncertainty.

The MSCI index, which tracks stocks in the Asia-Pacific region (excluding Japan), ended a seven-day rally and was down 0.15% on Thursday. The morning gains, triggered by Beijing's new measures to support the market, failed to hold until the end of the trading session.

Faced with threats from the US, China has taken its own steps to stabilize its stock market. The government has announced plans to channel hundreds of billions of yuan through state-owned insurers to support stocks.

These moves have had an effect: indexes in China have shown modest gains. The blue-chip CSI300 Index rose 0.19%, while the Shanghai Composite Index gained 0.53%. However, some of these gains were lost by the end of the session, highlighting the continuing nervousness of market participants.

Trump's investment plan has sparked enthusiasm in global markets, but tensions over tariffs on Chinese imports are becoming a restraining factor. Beijing, in turn, has demonstrated a willingness to protect its economic interests, which has helped temporarily strengthen the position of Chinese indexes.

The question of whether Trump's AI initiative can offset the potential fallout from a tariff war remains open.

Global markets are at a crossroads. Investors are weighing the potential of major AI initiatives, but are also keeping an eye on the risks associated with a tightening trade relationship. Macroeconomic data, corporate earnings, and international trade developments will be key drivers in the coming days.

Global markets continue to react to economic and political challenges. While Asian indices are mixed, China faces economic challenges, exacerbated by external threats from US tariffs.

Hong Kong's Hang Seng Index fell 0.6%, reflecting continued investor concerns about the economic situation in China. Alvin Tan, head of Asian FX strategy at RBC Capital Markets, said weak Chinese stock returns and falling bond yields are indicators of domestic challenges. "China is increasingly dependent on net exports for growth, and if the US ratchets up tariff pressure, these problems will only get worse," Tan said.

Meanwhile, Japan's Nikkei Index rose 0.8%. SoftBank shares were among the leaders, soaring 5%. The reason was the announcement of a joint project with OpenAI called Stargate AI. According to sources, each of the parties will allocate $19 billion to finance the initiative, which strengthened investor confidence in the Japanese conglomerate.

Movement in FX markets was relatively subdued after the instability caused by Donald Trump's plans to impose tariffs. The US President confirmed the possibility of 25% duties on Mexican and Canadian imports by February 1, which caused tension among market participants.

The US dollar index remained near a two-week low, ending the day at 108.26.

China's yuan weakened to 7.2812 per dollar on the domestic market, reflecting investor concerns about the country's economy.

Along with threats against China, Trump continues to increase pressure on other countries. Potential tariffs on imports from Mexico and Canada, which could reach 25%, are adding to the nervousness. Experts say such measures could slow down global trade, exacerbating existing uncertainty.

Asian markets remain under pressure, balancing optimism over tech initiatives with concerns over rising trade tensions. Investors are focused on what the US and China will do next, and whether initiatives from major companies such as SoftBank and OpenAI can support market resilience. As tensions mount, markets are likely to remain volatile, awaiting the outcome of trade policy and decisions by major economic players.

Financial markets are showing caution amid upcoming central bank decisions and global economic risks. The dollar continues to strengthen, while commodity markets remain under pressure, reflecting the nervousness of participants.

The American currency reached a one-week high against the yen, rising to 156.76. This rise is associated with expectations of a decision by the Bank of Japan, which may raise the rate by 25 basis points on Friday. Investors have already priced this into quotes, but attention is focused on the regulator's statement, which may provide more insight into the future course of monetary policy.

Norges Bank will announce its interest rate decision later on Thursday. Experts expect the Norwegian central bank to keep its key parameters unchanged, indicating how smaller economies are responding to global challenges.

World oil prices fell amid Donald Trump's threat of new tariffs. The proposal to impose additional duties has fueled concerns about a slowdown in global economic growth, which could in turn reduce demand for energy.

Market participants are concerned about the impact of potential trade restrictions on global supply chains and demand dynamics.

Amid volatility in the currency and commodity markets, the spot price of gold remains steady. An ounce of the precious metal still costs $2,754.49. This figure reflects the cautious behavior of investors who view gold as a safe haven asset in case of increased instability.

Markets are in a state of anticipation, analyzing the impact of both monetary decisions and possible tariff changes. The focus remains on the actions of central banks, especially the Bank of Japan, as well as the next steps of the Trump administration.

For commodity markets, supply and demand data will be key factors, as well as the development of trade negotiations. As long as investors remain cautious, volatility may persist throughout the week.

You have already liked this post today

*The market analysis posted here is meant to increase your awareness, but not to give instructions to make a trade.